1Q26 Quarterly Market Review

Quarterly Market Review

The first quarter of 2026 was a reminder that markets can look calm right up until they don’t. The year began on solid footing, but by late February, investors were dealing with rising geopolitical tensions, shifting rate expectations, and a market that had already priced in a lot of optimism. Headlines got heavier, oil moved higher, volatility picked up, and stocks gave back some ground after starting near record levels.

But markets don’t need perfect conditions to keep functioning, and long-term investors don’t need every quarter to be smooth for a plan to still work. What matters is understanding what actually happened, what likely mattered less than the headlines suggested, and how to stay the course when short-term market moves start pulling for an emotional reaction.

What We'll Cover

Key Takeaways

Geopolitical tension and rising oil prices added pressure during the quarter, but market moves were still shaped by a broader mix of inflation, interest rates, and investor expectations.

Stocks repriced as optimism gave way to caution, with returns diverging sharply across sectors and international markets offering a different pattern than the US.

Bonds reminded investors that higher yields come with price movement, but they also continued to offer more income than they did for much of the last decade.

The bigger risk wasn’t volatility itself. It was the temptation to react to it. A disciplined plan still matters more than a smooth quarter.

What the Headlines Don’t Show

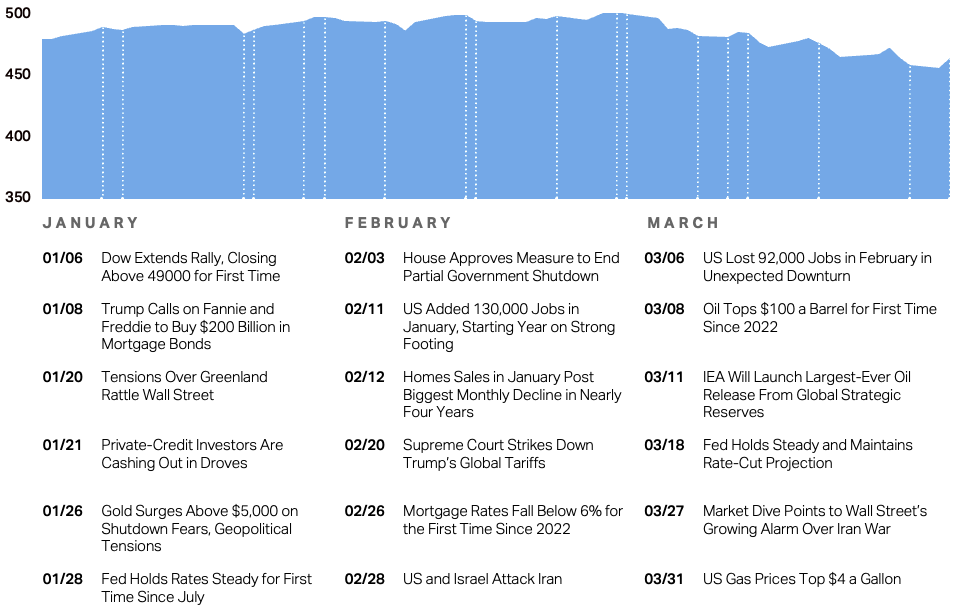

MSCI All Country World Index with selected headlines from 1Q26

These headlines aren't offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

Past performance is not a guarantee of future results.

In USD. MSCI All Country World Index, net dividends.

MSCI data © MSCI 2026, all rights reserved.

Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Headlines are sourced from various publicly available news outlets and are provided for context, not to explain the market's behavior.

How Markets Performed

Returns as of March 31, 2026

Tug of War

Stocks Repriced

Stocks spent the quarter in a restless tug of war between confidence and caution. When investors felt better about growth and earnings, the market responded quickly. When inflation, interest rates, or geopolitical tension came back into focus, optimism faded just as fast. That kind of movement can feel unsettling, but it’s normal in a market that’s constantly repricing what comes next.

Performance across sectors diverged sharply. Energy companies benefited from supply disruptions, while technology and consumer discretionary stocks were hit the hardest. The large technology leaders that previously drove the market were among the biggest individual detractors this time. While US stocks struggled, broad developed and emerging markets proved more resilient. For the disciplined investor, the lesson isn’t to hunt for a handful of winners. It’s to own a portfolio that doesn’t depend on one narrow part of the market to do all the heavy lifting.

Bonds Still Matter

Bonds continued their shift back toward being a genuine source of income and stability, but they also reminded investors that prices still move when inflation expectations change. The spike in energy costs tied to geopolitical tensions kept inflation concerns front and center. That’s not a failure. It’s how bonds work while the market figures out where rates will settle.

The better news is that higher yields have made bonds more productive again. Income now carries more of the return load than it did for much of the last decade. That matters for retirees, near-retirees, and anyone who needs the bond side of a portfolio to do more than just sit there. Bonds don’t need to be exciting to be useful. Their job is to add stability, support cash flow needs, and give the rest of the portfolio room to work.

A Slower, More Normal Economy

The economy kept sending mixed but familiar signals. Households continued to spend, and the labor market was still holding up. At the same time, the cheap money era of the previous decade is firmly in the rearview mirror. Inflation remained above preferred levels, and the Federal Reserve held rates steady. This has reduced expectations for future rate cuts.

Higher borrowing costs and elevated energy prices are showing up in real decisions people and businesses make. Even when inflation cools, the path is rarely a straight line. Since inflation influences interest rates, and rates influence everything from mortgage payments to stock valuations, markets kept reacting quickly to new data.

For you, the point is simple. A good plan doesn’t require a perfectly predictable economy. It requires a portfolio built to handle a range of outcomes and a decision-making process that’s slower than the news cycle.

Reaction Is The Risk

Much of the lasting damage doesn’t come from the market itself. It comes from how investors react to it. People get cautious after declines, then confident again after recoveries. That’s one of the easiest ways to buy high and sell low without meaning to.

There’s a more subtle version of this problem. Investors start treating their portfolios like commentaries on their intelligence. When markets rise, they feel smart. When markets fall, they feel wrong. That emotional loop can lead to constant tinkering, unnecessary taxes, added costs, and a portfolio that’s always chasing certainty that never really arrives.

What gets lost in these moments is that markets are supposed to move. They’re supposed to respond to new information. Not every geopolitical event or oil spike leads to a lasting change in long-term outcomes. However, reacting to each one as if it does can create exactly that outcome.

A good plan already accounts for uncertainty. It assumes there will be periods where discipline feels uncomfortable. It builds in the expectation that markets won’t move in a straight line. The goal isn’t to avoid those moments. It’s to have a process you can follow when you’re in them.

Looking Ahead

The next quarter will bring new headlines, and some of the same ones will carry forward. Interest rates will still matter. Inflation will still matter. Growth expectations will still matter. But none of those are reasons to treat your portfolio like a short-term opinion. There are reasons to stay focused on what you can control, like spending, savings, taxes, diversification, and the level of risk you’re actually willing to live with.

The more important question right now isn’t where stocks or bonds go next. It’s whether your financial life is set up to help you avoid costly mistakes. That means having enough cash for near-term needs, keeping debt and fixed expenses at a level that doesn’t trap you, and making sure your investment risk matches your timeline. When those pieces are in place, market volatility becomes something you experience, not something you have to solve.

What Actually Matters

There’s nothing in this quarter that requires a change in strategy. This environment is exactly what your plan was built for.

What worked best in the first quarter wasn’t a clever prediction. It was having a framework. We’re seeing diversification matter again, with more areas of the market contributing and bonds playing a more useful role. Higher interest rates, while frustrating in some ways, are also creating better income opportunities. The economy is holding up better than many expected.

Your plan isn’t designed for ideal scenarios only. It’s designed to handle real conditions, including ones like this. That isn’t a flaw in the plan. It’s the whole point.

In practical terms, last quarter reinforced a few basics. Keep emergency reserves separate from long-term investments. Don’t let a recent winner become a concentrated part of your future. Rebalance when it’s uncomfortable, not when it feels obvious.

If your plan is built around long-term goals, your portfolio should be built to tolerate short-term discomfort.

Disclosures

All expressions of opinion reflect the judgment of the author(s) as of the date of publication and are subject to change. The content on this blog is for informational and educational purposes only and should not be construed as personalized financial advice, tax advice, legal advice, an offer or solicitation to buy or sell any security, or a recommendation to pursue any specific investment strategy. The information provided is general in nature and may not be suitable for your individual circumstances.

Olio Financial Planning, LLC (“OLIO”) is a registered investment adviser with the United States Securities and Exchange Commission, domiciled in Virginia. Investment advisory services are only provided to investors who become OLIO clients under a written agreement. Past performance does not guarantee future results, and all investments involve risk, including the potential loss of principal.

Nothing contained herein should be interpreted as a guarantee of any specific outcome. Forward-looking statements or projections are based on assumptions and current market conditions, which are subject to change without notice. Actual results may differ materially.

You should consult your own financial, legal, tax, or other professional advisors before making any financial decisions. OLIO does not guarantee that the information presented is current, accurate, or complete, and assumes no responsibility for any errors or omissions.