Part II: The Mix That Matters

Part II:

Asset Allocation —

The Mix That Matters

What We'll Cover

The Mix Moves the Needle

When it comes to investing, not all decisions carry equal weight. Research shows that the vast majority of long-term investment outcomes don’t come from picking the perfect stock or perfectly timing the market.

Instead, it comes down to one key decision: how your money is allocated. To be clear — we’re talking about portfolio behavior. The swings, the ups and downs, not just total return.

A landmark study by Brinson, Hood & Beebower found that over 90% of return variability across institutional portfolios came from asset allocation. Not market timing or security selection.

Not what you bought. Not when you bought it. But how the pieces work together.

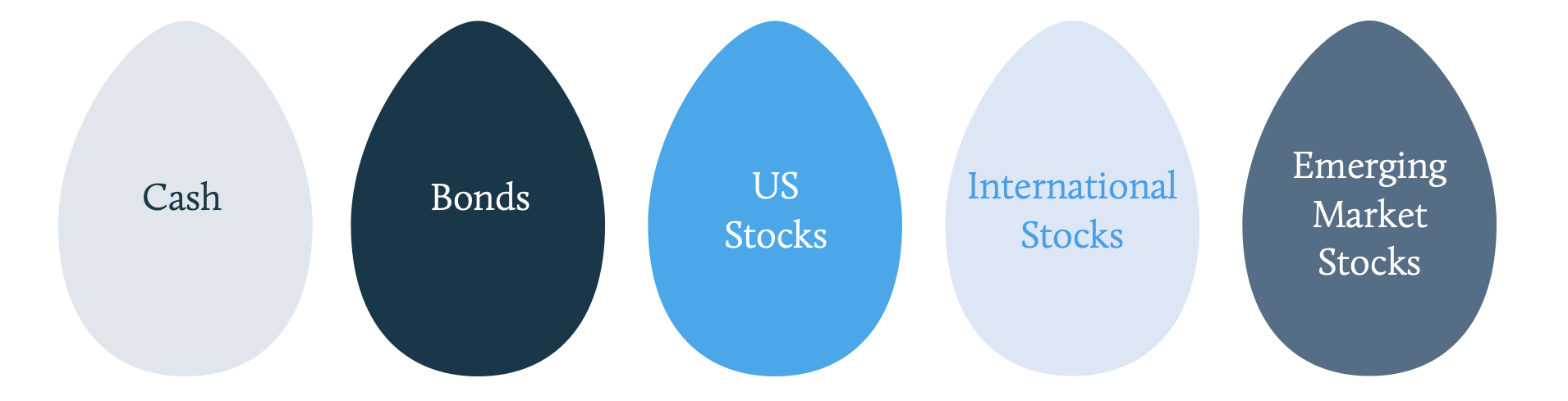

That’s the core of it. Your mix of cash, bonds, stocks, and other asset classes drives the experience of your portfolio more than anything else.

Why Asset Allocation Matters

Your portfolio is like a recipe. Too much of one ingredient can throw off the whole dish. Asset allocation is how we strike the right balance — enough liquidity, enough stability, enough growth to reach your goals without taking on unnecessary risk.

Diversification isn’t just a buzzword. It’s a Nobel Prize — winning idea. In 1952, economist Harry Markowitz introduced Modern Portfolio Theory, showing that combining investments that behave differently can reduce risk without lowering expected returns. That principle still shapes how portfolios are built today.

When determining the right mix of asset classes, each one has distinct characteristics in terms of risk and return, should demonstrate long-term profitability across market cycles, and ideally won’t move in lockstep with the others — meaning lower correlation and a smoother ride.

It’s not about avoiding risk. It’s about spreading it out — so you can stay invested through the ups and downs.

Modern Portfolio Theory (MPT) remains one of the most widely accepted frameworks for building diversified investment portfolios. Developed by economists Harry Markowitz and William Sharpe, both recipients of the Nobel Prize, MPT laid the foundation for how we understand the relationship between risk and return.

While MPT has its limitations, we believe it’s the strongest foundation to build a compelling, disciplined investment strategy — one designed to align with your goals and hold up over time.

Diversification is the only free lunch in investing.

Beyond the Basket

You’ve heard it before: “Don’t put all your eggs in one basket.” But diversification is more than that. It’s about owning the right things in the right amounts. It’s not just being diversified across different companies, but also across different asset classes. A well-diversified portfolio includes investments that behave differently in various market conditions.

It also means avoiding concentration risk. As a general guideline, no individual stock should represent more than 5% of your portfolio.

Why?

The table below shows Fortune’s “Most Admired” Companies of 1999 alongside their subsequent 20-year returns. The average performance of this group underperformed the S&P 500 Index by 80.5%.

| Company | Absolute Return | Relative Return |

|---|---|---|

| General Electric | -47.2% | -275.3% |

| Microsoft | 358.8% | 130.7% |

| Coca-Cola | 177.2% | -50.9% |

| Intel | 147.6% | -80.5% |

| Berkshire Hathaway | 362.6% | 134.5% |

| IBM | 55.7% | -172.4% |

| Walmart | 226.7% | -1.4% |

| Cisco | 114.4% | -113.7% |

| Dell | -59.7% | -287.8% |

| Merck | 139.7% | -88.4% |

| Average | 147.6% | -80.5% |

| S&P 500 | 228.1% |

Source: O'Shaughnessy Asset Management. Data from July 1999 through June 2019

Getting the Mix Right

In Part I of How do you choose the investments in my portfolio?, we started with the question that guides it all: What do you need your money to do? Your answer sets the direction for every decision that follows.

From there, we align your investment mix with your goals, your time horizon, and your comfort with risk to balance stability, income, and growth in a way that fits your life.

We use forward-looking research and simulate thousands of possible market outcomes to build a strategy designed to hold up now and later.

Because at the end of the day, it’s all about the mix.

Cash keeps things liquid when you need them.

Bonds can provide income and smooth out the ups and downs.

Stocks can help grow your money over time.

But the mix depends on timing.

Investing in stocks to buy a car in two years is very different than investing in stocks to retire in twenty. For example, someone who invested in 2007 and needed the money by 2009 likely saw losses from the financial crisis. But if they had seven or more years, that same investment had time to recover and grow.

Risk isn’t just about market swings.

It’s about whether your money will be there when you need it. That’s why we don’t just diversify—we plan intentionally, based on what your money is for, both now and in the future.

Your Allocation Moves With the Moment

You won’t have the same mix forever.

As your life evolves, so should your investments. That’s why we don’t just set your allocation and forget it. We revisit your portfolio regularly to make sure it still reflects your goals, time horizon, and risk comfort — not just when the markets move, but when you do.

Because what made sense five years ago might not make sense today. And what fits today might need to change tomorrow.

An example of income growth assets is stocks, and an example of income risk management assets is bonds. Investing involves risks, including possible loss of principal. Bonds are subject to increased loss of principal during periods of rising interest rates and may be subject to various other risks, including changes in credit quality, liquidity, prepayments, and other factors. There is no guarantee investment strategies will be successful or that a desired goal or objective will be achieved.

Aligned, Not Just Invested

If your investment objective is the why, then asset allocation is the how. It’s not about being perfect — it’s about being prepared. Positioned to capture long-term growth without taking more risk than you need.

You don’t need to memorize formulas or run simulations. That’s our job.

Your job? Know your goals. Give it time.

Because good investing isn’t about precision — it’s about alignment.

With your goals. Your timeline. Your life.

And when you’re aligned, you’re positioned.

To stay the course.

To adapt when life changes.

To grow, not guess.

Disclosures

The content on this blog is for informational and educational purposes only and should not be construed as personalized financial advice, tax advice, legal advice, an offer or solicitation to buy or sell any security, or a recommendation to pursue any specific investment strategy. The information provided is general in nature and may not be suitable for your individual circumstances.

Olio Financial Planning, LLC (“OLIO”) is a registered investment adviser with the United States Securities and Exchange Commission, domiciled in Virginia. Investment advisory services are only provided to investors who become OLIO clients under a written agreement. Past performance does not guarantee future results, and all investments involve risk, including the potential loss of principal.

Nothing contained herein should be interpreted as a guarantee of any specific outcome. Forward-looking statements or projections are based on assumptions and current market conditions, which are subject to change without notice. Actual results may differ materially.

You should consult your own financial, legal, tax, or other professional advisors before making any financial decisions. OLIO does not guarantee that the information presented is current, accurate, or complete, and assumes no responsibility for any errors or omissions.